Executive Summary

In boardroom energy procurement, the lowest tariff on paper is often the most expensive mistake in reality.

When the CFO of a massive FMCG company in Andhra Pradesh began evaluating Open Access Renewable Energy solutions, the objective was simple: secure the lowest possible Power Purchase Agreement (PPA) rate.

Facing a ₹17.90 Crore annual grid OPEX and looming CBAM (Carbon Border Adjustment Mechanism) taxes, he shortlisted two developers.

Developer 1 offered a pure Solar PPA at ₹3.75/unit. Developer 2 offered a Solar + Battery Energy Storage System (BESS) at ₹3.92/unit, demanding an additional ₹49 Lakhs in upfront equity.

To a traditional procurement mindset, signing the ₹3.92 PPA sounds like financial suicide. But by running a forensic Techno-Commercial audit, we proved that the “cheaper” L1 tariff was actually a trap that would have stranded the company’s capital.

Here is the exact mathematical framework we used to justify paying a premium tariff to generate maximum net wealth.

The Dilemma: High Burn & Strict Mandates

Before evaluating the PPAs, we had to isolate the exact problem on the company’s balance sheet. The FMCG manufacturing plant was in a tight spot:

- The High Burn: The facility was consuming 3.00 Crore grid units annually, bleeding ₹17.90 Crore in pure operational expenses (OPEX).

- The Financial Mandate: The Board had strictly mandated a direct power cost reduction of at least ₹2/unit for FY26.

- The ESG Threat: Global buyers were mounting intense pressure to hit maximum RE replacement by 2027 to avoid severe CBAM export taxes.

Driven by these constraints, the CFO naturally leaned toward the lowest possible PPA tariff.

The L1 Tariff Trap: Why “Cheaper” Fails

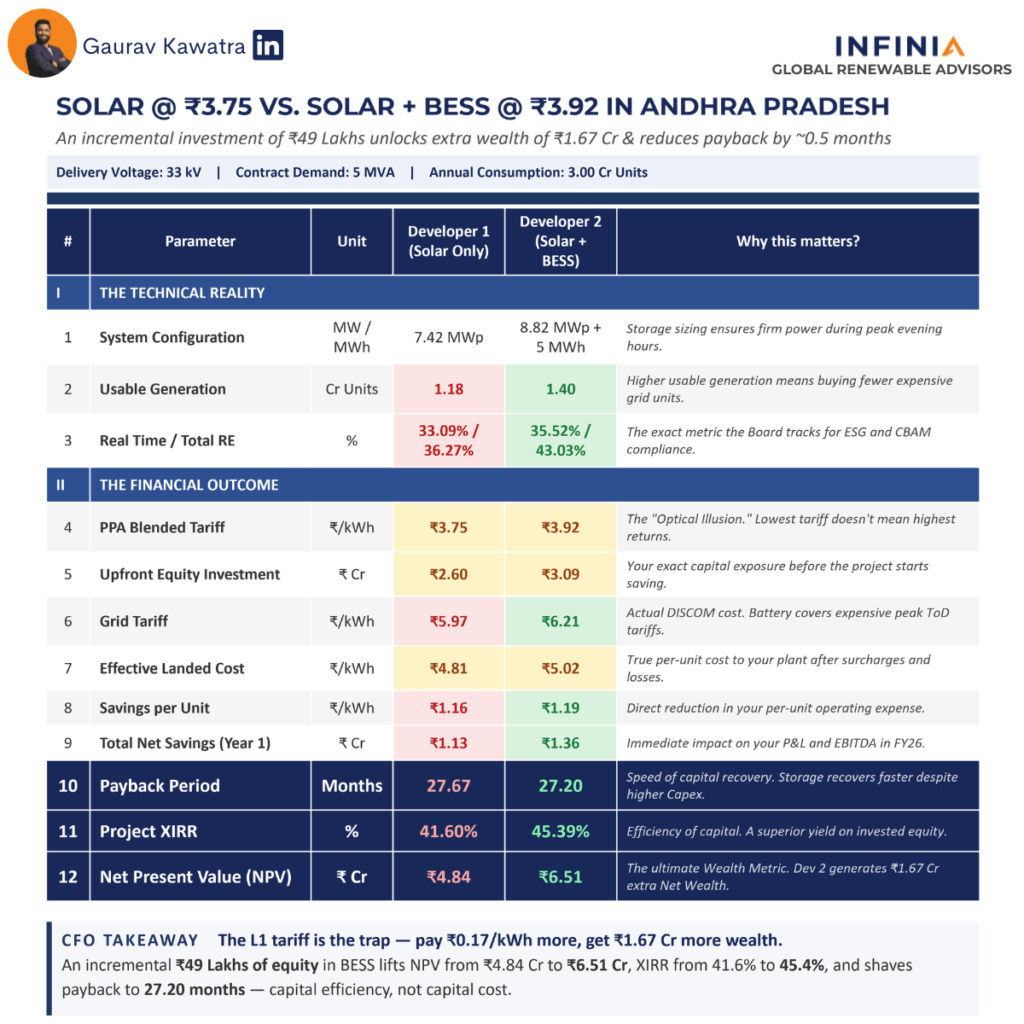

The CFO was ready to sign a Term Sheet with Developer 1, who offered a standard Solar Only solution at ₹3.75/unit and required a lower equity investment of ₹2.60 Crore.

But before presenting this to the Board, he asked us to independently audit the numbers. Our forensic analysis exposed the fatal flaw in the standard solar model: The Generation vs. Consumption Curve.

Because solar only generates during specific daytime hours, the plant could not absorb all the power it produced.

- The Savings Reality: After accounting for Andhra Pradesh’s specific landed costs and cross-subsidy surcharges, the true savings were only ₹1.16/unit—completely failing the Board’s ₹2/unit mandate.

- The Wasted Power: Due to the solar generation curve, the plant could only actually use 1.18 Crore units.

- The Result: The plant would only achieve a 36.27% Total RE Replacement and a highly inefficient 33.09% Real-Time Replacement.

The BESS Premium: Engineering True Capital Efficiency

We then evaluated Developer 2, who offered a Wind-Solar Hybrid + BESS solution at ₹3.92/unit. This structure demanded a higher equity investment of ₹3.09 Crore (an additional ₹49 Lakhs upfront).

Why would any CFO agree to this? Because the Battery Energy Storage System acts as a shock absorber, shifting unusable daytime power to high-tariff evening peaks.

- The Generation Jump: By integrating BESS, the total usable generation spiked from 1.18 Crore units to 1.40 Crore units.

- The Result: Total RE Replacement jumped to 43.03%, and Real-Time Replacement rose to 35.52%.

The Verdict: The Math That Convinced the Board

The CFO took this forensic data to the Boardroom. It was an absolute no-brainer to sign with Developer 2, despite the higher PPA tariff and the extra upfront equity.

When you stop looking at the PPA tariff and start looking at true capital efficiency, Developer 2 was the undisputed winner:

- The Payback Accelerated: Despite investing ₹49 Lakhs more, the payback period dropped from 27.67 months down to 27.20 months.

- The XIRR Spiked: The project XIRR jumped from an already strong 41.60% to a massive 45.39%.

- The Net Wealth (NPV) Exploded: Most importantly, the Net Present Value of the project over its lifetime grew from ₹4.84 Crore to ₹6.51 Crore.

The Board approved the higher equity and the ₹3.92 tariff unanimously.

Next Steps for the C-Suite

If your company is evaluating an Open Access Term Sheet, do not fall into the L1 Tariff Trap. A cheaper per-unit cost on paper often results in millions of wasted units and stranded capital in reality.

If you want us to run a Techno-Commercial Wealth Audit to stress-test the real NPV, XIRR, and usable generation of your proposed Solar or Hybrid project before you commit your capital:

In this session, we will audit your exact financial model so you can walk into your next Board meeting with a mathematically unassailable energy strategy.

About Infinia Solar

Infinia Solar is India’s leading renewable energy consultant.

We help Commercial and Industrial consumers procure the right renewable energy solutions, from the right developers, and on the right PPA terms.

We’ve served 60+ customers across 18 states, enabling 1.4 GW of open access and rooftop solar capacity, and have facilitated 150+ PPAs so far.

This has helped our customers reduce up to 50% of their electricity costs and replace up to 100% of their power with renewable energy.

We have also collaborated with 50+ developers, and our customers fondly refer to us as the ‘Amazon of the renewable energy industry.‘