Executive Summary

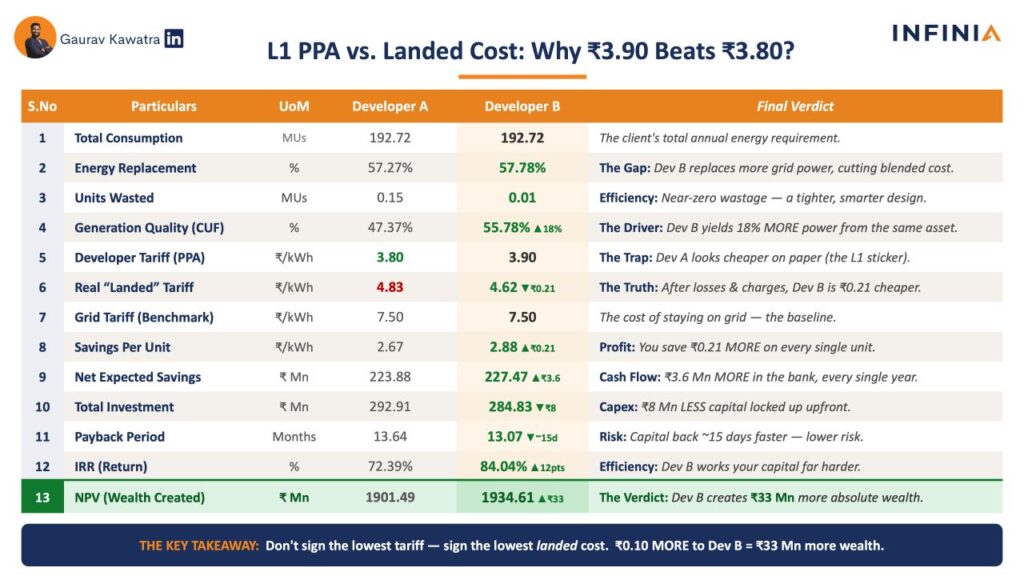

A Chemical Giant in Gujarat was bleeding capital with a grid tariff of ₹7.50 per unit. Under pressure to switch to Green Energy for their 192 Million Unit consumption, the CFO shortlisted two developers. Developer A offered the lowest L1 tariff at ₹3.80. Developer B offered ₹3.90. The obvious choice was Developer A. I forced the client to sign the more expensive ₹3.90 PPA. This post breaks down how the “cheapest” sticker price was a financial trap, and how prioritizing Capacity Utilization Factor (CUF) over the L1 tariff created ₹193.46 Crore in Net Present Value (NPV) and ₹3.3 Crore in extra savings.

The Setup: The “L1” Illusion

The pressure on the CFO was massive. Investors demanded an immediate switch to Green Energy to decarbonize operations and reduce the crippling ₹7.50/unit grid costs. After months of intense negotiations, the boardroom had two finalists on the table:

- Developer A: Offered a ₹3.80 tariff with a 47.37% CUF.

- Developer B: Offered a ₹3.90 tariff with a 55.78% CUF.

Looking at the plain vanilla proposal, the CFO was ready to sign with Developer A. It was the L1 bid. It was mathematically the cheapest on paper. It looked like a guaranteed win for the Board.

I stopped him. I told him: “Don’t fall for the Sticker Price. Look at the Replacement.”

The Constraint: The Hidden Grid Trap

When we ran our Techno-Commercial Analysis, the reality of the ₹3.80 bid surfaced.

The “cheap” option (Developer A) only had a CUF of 47.37%. The trap is simple but lethal: whatever power the developer cannot supply, the client is forced to buy from the grid at the exorbitant rate of ₹7.50.

The “expensive” option (Developer B) had a significantly higher CUF of 55.78%. By paying just ₹0.10 extra to the developer, the client would avoid buying millions of units from the expensive grid.

The Verdict: Landed Cost Beats Sticker Price

The boardroom math shifted entirely when we stopped looking at the base tariff and started looking at the actual Landed Cost. We proved that Developer B delivered a vastly superior financial outcome:

- Higher Net Present Value (NPV): ₹193.46 Crore in absolute wealth created.

- Faster Payback Period: Capital recovered in just 13.07 months.

- Extra Cash Flow: ₹3.3 Crore in additional savings over the PPA tenure.

They signed at ₹3.90. The Board applauded the decision.

The lesson for every CXO is that the naked eye cannot see the L1 trap. A plain vanilla ₹3.80 vs. ₹3.90 comparison will destroy your balance sheet if you do not account for replacement power. You must make decisions based on NPV, Payback, and CUF.

Next Steps for the C-Suite

If you are a Corporate Energy Consumer stuck in the “Developer Shortlisting” phase, do not sign based on the L1 sticker price.

You need to stress-test your developer’s CUF claims and calculate your true Landed Cost before presenting it to your Managing Director.

In this session, my team and I will run a detailed Techno-Commercial Analysis on your shortlisted bids and deliver a PPT-ready framework to ensure your energy strategy is mathematically unassailable.

About Infinia Solar

Infinia Solar is India’s leading renewable energy consultant.

We help Commercial and Industrial consumers procure the right renewable energy solutions, from the right developers, and on the right PPA terms.

We’ve served 60+ customers across 18 states, enabling 1.4 GW of open access and rooftop solar capacity, and have facilitated 150+ PPAs so far.

This has helped our customers reduce up to 50% of their electricity costs and replace up to 100% of their power with renewable energy.

We have also collaborated with 50+ developers, and our customers fondly refer to us as the ‘Amazon of the renewable energy industry.‘